Contra Krugman’s Eurocope: Yes, Europe is declining relative to the U.S.

Economic excuses are a recipe for further overdependence on the U.S. and a weak European contribution to global innovation

Paul Krugman has been “Challenging the Narrative of European Decline” again. I am struck because he is making essentially the same argument as 25 years ago. But while the data in 2001 might have been ambiguous, developments since then have not been.

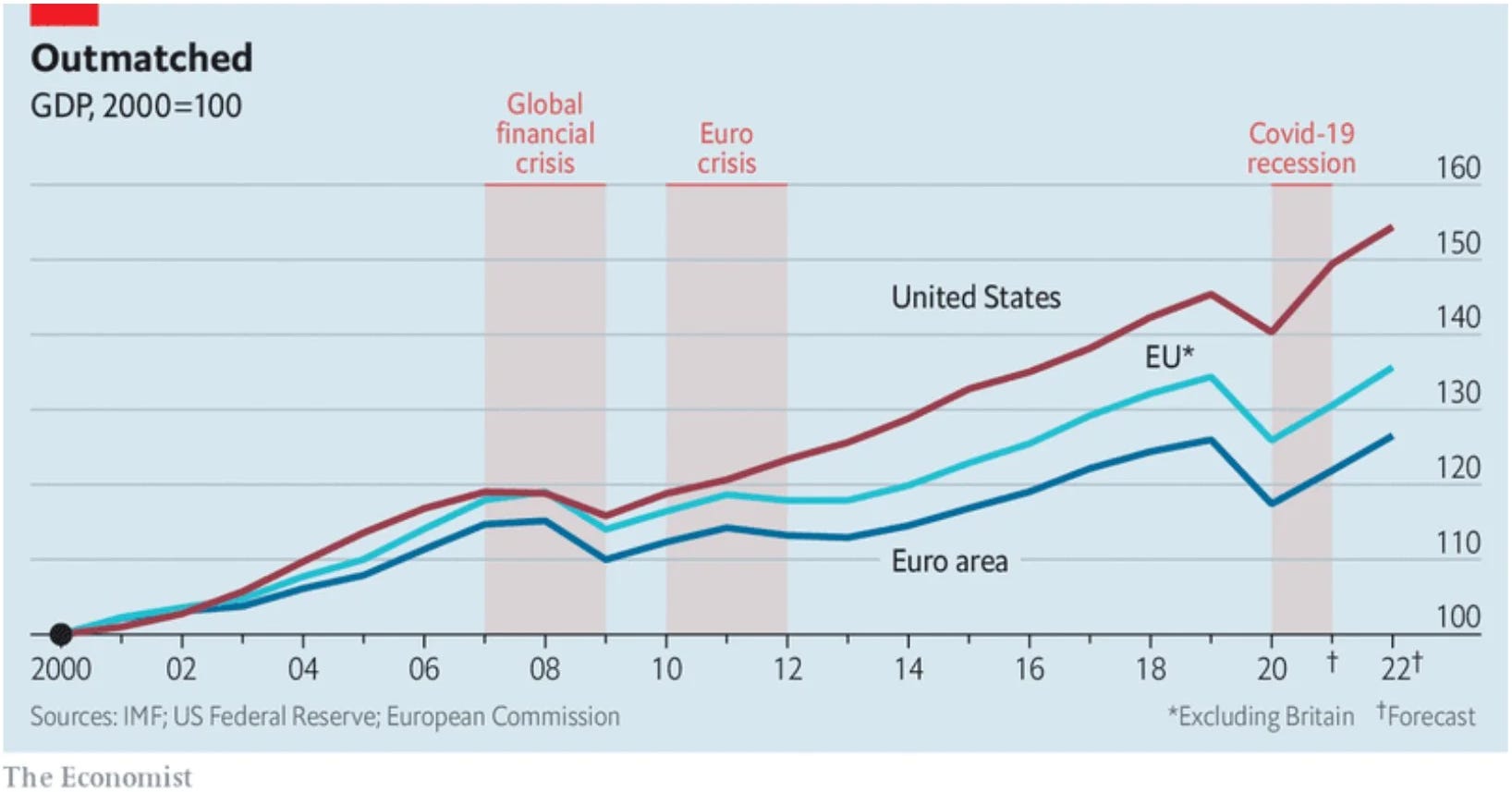

The transatlantic growth gap has become abyssal, growing deeper with every crisis the EU lurches through (the following chart does not include developments since the Ukraine War):

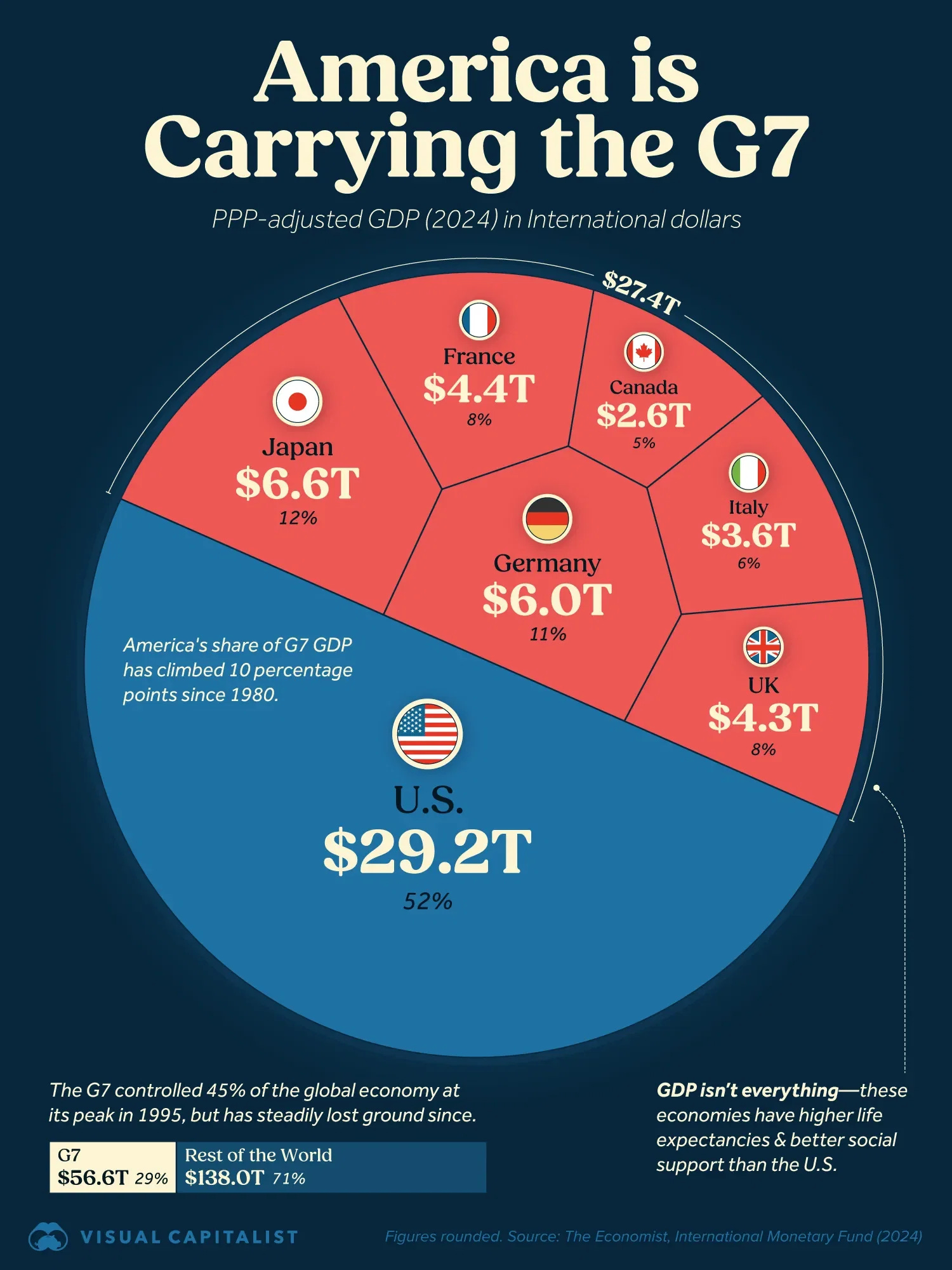

As a result of European and Japanese stagnation, the U.S. economy now makes up more than the rest of the G7 put together. That’s a 10 percentage point increase (42% to 52%) since 1980.

America’s decisive edge has been growing thanks to the combination of high productivity (unlike Japan), relatively high working hours (unlike Western Europe), and a growing population, notably through immigration and fertility. The U.S. population has increased by 62 million since 2000, almost as much as the whole population of France. What’s more immigration to Europe is often a net negative fiscally (as documented in Denmark, the Netherlands, and Finland), due to a combination of low human capital, lower employment and tax contributions, and higher welfare use.

Krugman argues that U.S. productivity (output per hour) hasn’t further increased relative to Europe’s, so who cares if its economy is growing more? Well, there are innumerable benefits to a larger economy. One is that a bigger economy gives you more resources to project your power on the world stage. The EU’s comparative weakness means more humiliating dependence on the United States in military, financial, technological, and other areas.

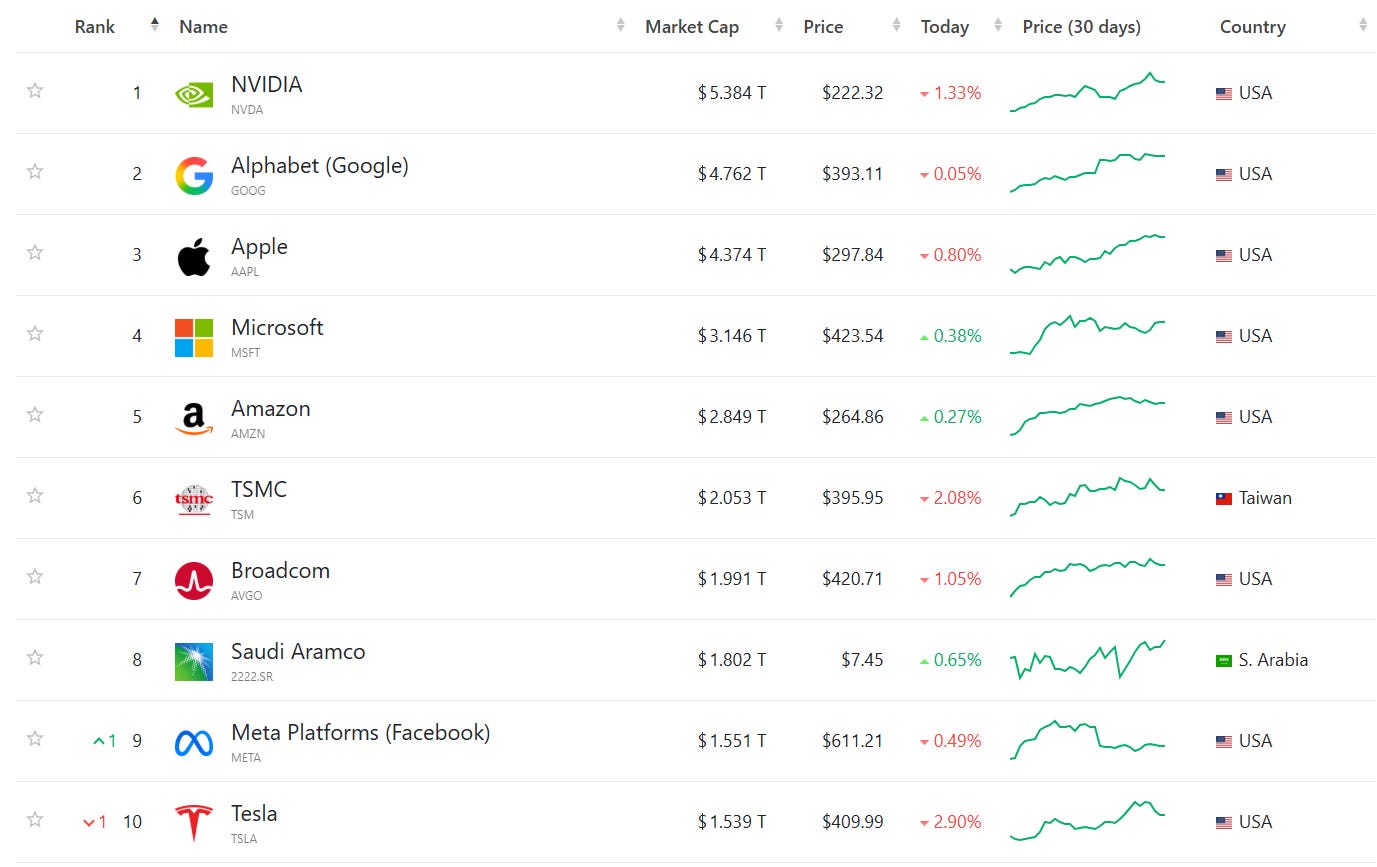

American economic dominance is shown by any number of metrics. Take the 10 biggest companies worldwide by market capitalization:

Besides the Netherlands’ ASML at #21, you have to go way, way down the list to start finding European companies. It is striking that the now dominant U.S. companies are often young (Nvdia founded 1993, Tesla 2003…), the European companies tend to be old (e.g., France’s L’Oréal founded in 1909, Germany’s Siemens 1847). Big European companies tend to maintain positions in mature sectors—sometimes thanks to holding more or less captive national markets—rather than break through creating new sources of wealth in emerging industries.

This isn’t just vibes. Consider the distribution of Unicorns—start-ups valued at over $1 billion: the U.S. and China simply dominate, while Europe (especially outside the UK) is essentially a no man’s land. This was to the state of things a decade ago:

Ten years later, Continental Europe hasn’t produced a single one of the world’s top 30 Unicorns by value:

This outcome isn’t terribly surprising:

Europeans have less spare cash to invest than Americans.

Europeans see limited upside to investment because of high taxes and their market often being fragmented for new industries.

There is also massive downside risk to any adventurous investment because of massive liabilities if ever you need to fire workers, due to the punitive labor laws in most of western Europe.

By contrast, it is perfectly rational for Americans to make bold investments in new industries even if most don’t pay off: one big winning investment can easily recoup all your losses.1

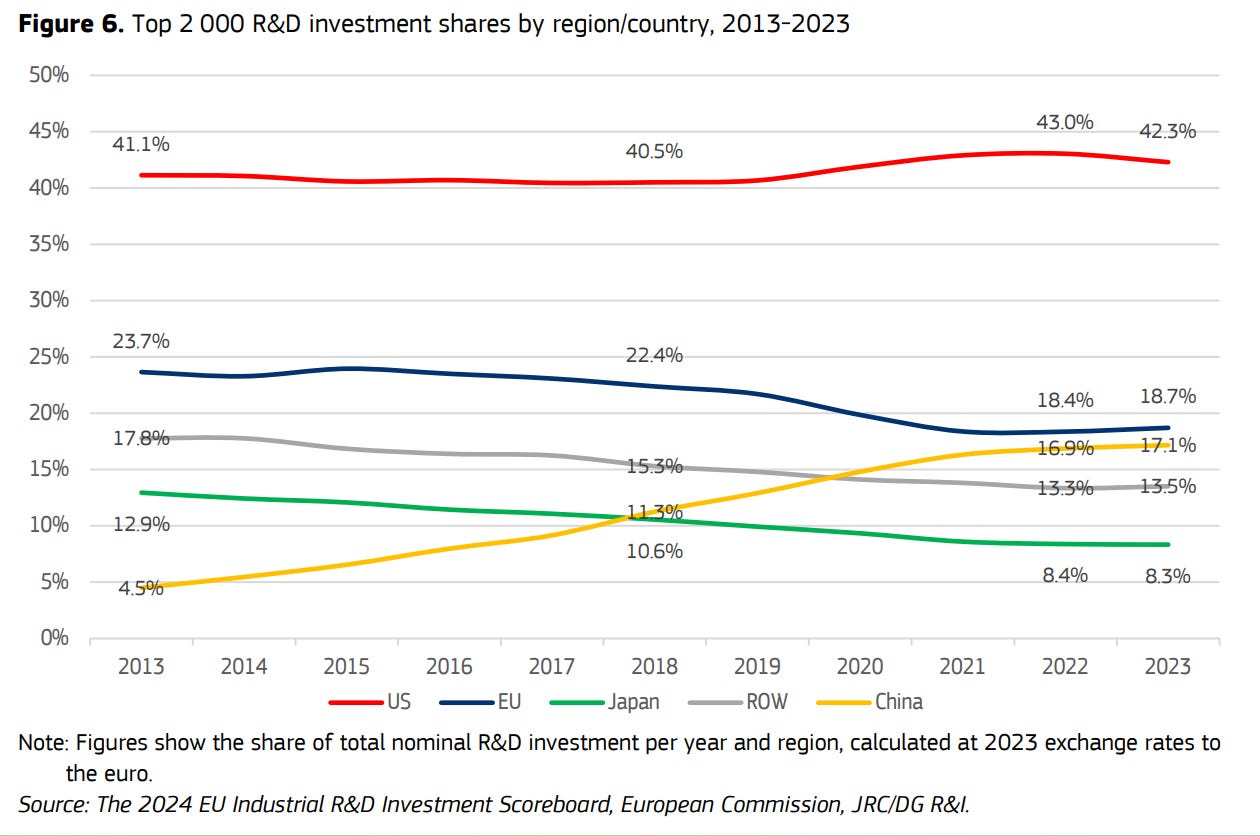

A growing economy driven by innovation and venture capital also means more contributions to global public goods. European Commission research shows that the U.S. dominates the share of R&D investment among the world’s top 2000 companies. The U.S.—with less than 4.5% global population—consistently accounts for over 40% of global R&D! Since 2013, the EU has fallen below 20% and Japan below 10%, while China has risen spectacularly.

I think the argument from innovation is fundamental. I even think it is a moral argument. At the end of the day, all human progress depends on the innovations made by minorities whose benefits, to varying degrees, eventually spread to all humanity. Solving challenges like climate change, factory farming, and diseases will depend, above all, on innovation. To that extent, I would go so far as to argue that it is immoral for Europe (or any other region) to unnecessarily contribute less to global innovation due to misguided or selfish policies.

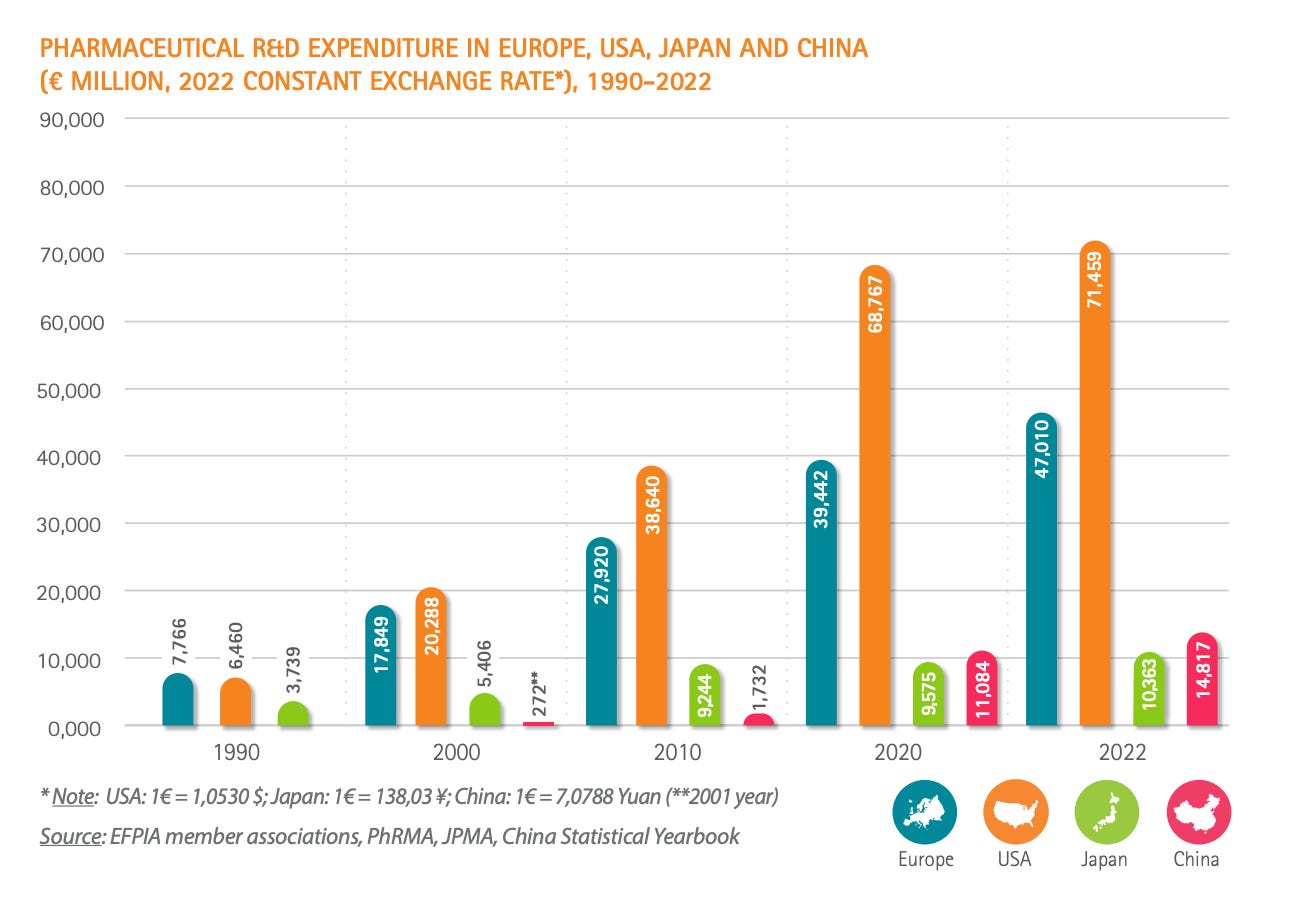

The R&D trend is confirmed in any number of industries. Here is the picture of medicines for example:

As recently as the 1990s, Europe (including the UK) actually did more pharmaceutical R&D than the U.S. Since then, the U.S. has massively increased investment to over 50% the European figure. There is considerable truth to the argument that U.S. consumers are subsidizing pharmaceutical innovation through high prices, while the rest of the world passively benefits from lower prices and/or eventual conversion into generics.

Krugman is right to say that Europeans are perfectly able to purchase, apply, and often copy American innovations. But is that really what Europeans should aspire to? To be comfortable and passive consumers of innovations produced by others? There is certainly a rather disturbing feeling in Europe that the world is passing us by, that the world of tomorrow will be defined by others—especially the Americans and the Chinese—while Europeans watch, “regulate,” and muddle through.

Krugman also tries to relativize Europe’s decline in other ways, such as by saying this decline is within the same bounds as that experienced by different U.S. states, so it’s not a big deal. Actually, the economic and associated demographic differentials among U.S. states are a big deal. It is significant that big blue states like California, New York, and Illinois have been losing population to emigration, while people have flocked to some big red states like Texas and Florida.

{kind=link}

This ability for economic self-correction by people voting with their feet is both one of the great sources of American dynamism and changes the character of the nation as a whole. Over time, more populous and richer states tend to get more overall national influence after all. (As was seen, for example, after the Founding, when free northern and western states significantly outgrew southern slave states.)

At the level of the world, Europe is simply becoming weaker while the U.S. more or less sustains its elevated position. Europe’s economic underperformance (along with its fertility collapse, aging, and unfunded pension/healthcare systems) is a chief culprit of this.

French Foreign Minister Jean-Noël Barrot recently breathlessly declared that “Europe will be the superpower of the 21st Century.”

As justification, he cited Europe’s higher quality of life (as desirable as this is, hardly relevant to superpower status) and its attractiveness to partners wary of U.S. and Chinese unilateralism. The latter is a real point but only gets you so far: the various middle powers the UK, Canada, Japan, South Korea, and Taiwan are all also declining relative to the U.S. and anyway don’t have a lot of cohesion as a group.

Barrot affirms: yes, Europe will be a superpower, we just have to continue President Emmanuel Macron’s decade-long fight for “European sovereignty.” The latter—referring essentially to more made-in-Europe industries to achieve “strategic autonomy”—is neither enough to be a superpower nor really possible on a dwindling economic base.

I am tempted to say power-political big talk on Europe is a common alibi of French politicians for failure to adopt domestic reforms addressing France’s decline. Why do necessary reforms at home if anyway we will be strong as part of “Europe”? This argument has been a staple of French leaders at least since the time of President François Mitterrand in the late 1980s, who did considerable damage to the French economy but offered young people and the better educated the horizon of “Europe.”

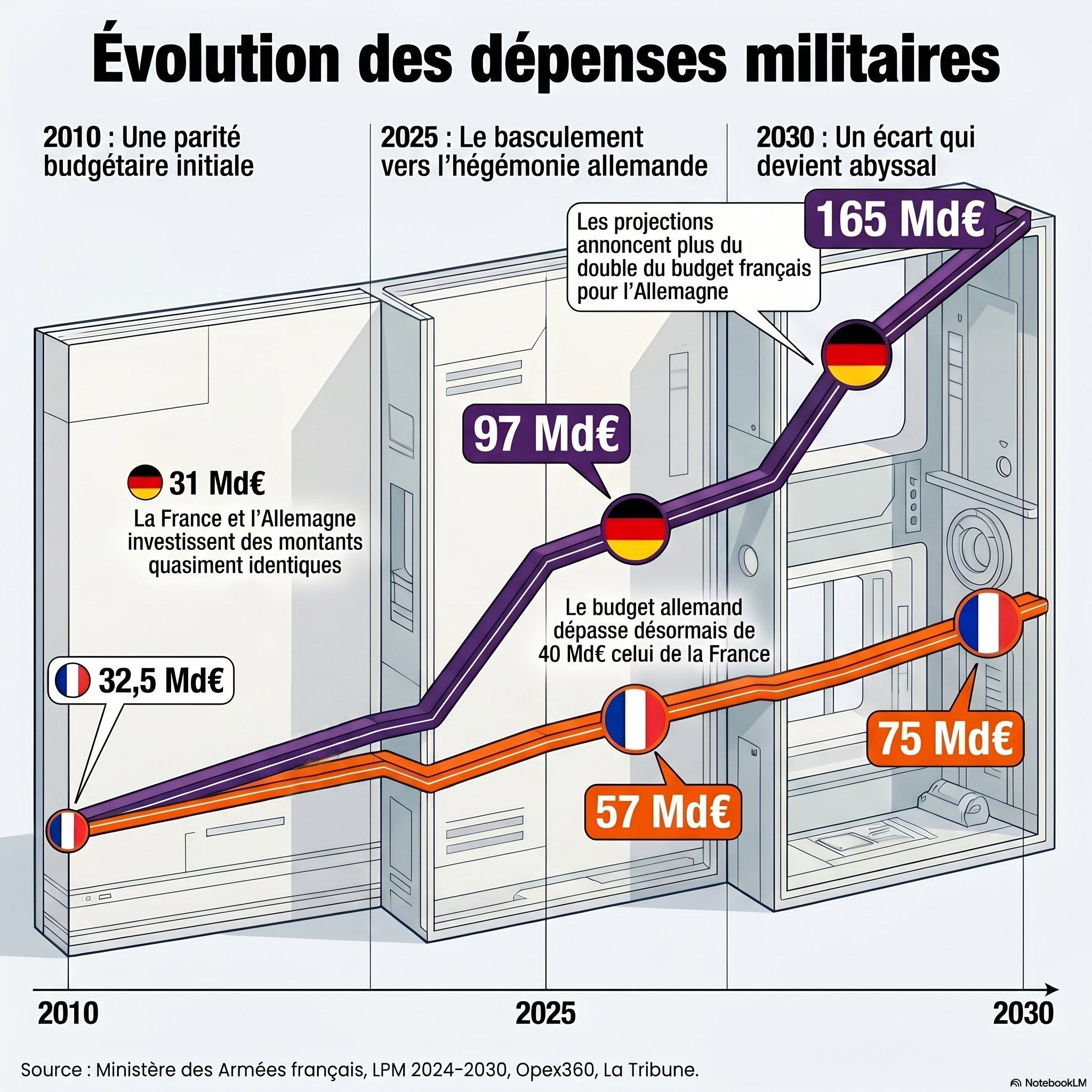

French power, however, is in stark decline. As I have argued elsewhere, the French debt outlook is catastrophic due to constantly rising overvalued pensions and a national consensus in French society (shared by nationalist and leftist parties supported by 2/3rds of the population) that the retirement age should be lowered back below 64. The European Commission forecasts France will reach an Italian-style level of public debt of 120% of GDP by 2027. It can never be repeated enough: low growth and national bankruptcy have serious geopolitical consequences: German defense spending will massively outpace France for the first time since the 1980s.

How to reverse Europe’s decline? It is by no means impossible in principle. Many of the needed actions have already been outlined in former European Central Bank President Mario Draghi’s famous report on competitiveness. The EU needs to be a place where it actually makes economic sense to make innovative investments. That means less taxes, more flexible labor, cheaper energy, a more cohesive single market, and abandoning overregulation and “precautionary” approaches (often simply technophobic) in sectors like biotech and data.

There are also spectacular national success stories, as with market-friendly Poland’s astonishing growth. Poland is now richer than several southern European countries and may well overtake some western countries.

At the end of the day, the world does not care about our feelings. Many console themselves with the thought that Europe’s high quality of life makes it superior to the U.S.

Certain peoples and powers persist and grow, and the world comes to reflect them more and more, while others decline or even fade away. Europe’s economic decline has real costs: more dependence on the fickle USA and an underpeforming European contribution to global innovation are perhaps the two most striking. Europeans deserve better than Krugman’s flattering excuses or Barrot’s wishful thinking: we need to do better.

For more data and arguments, I invite you to check out economist and former MEP Luis Garicano’s Substack. See also his case for how to restart growth in Europe.

I love U.S. Supreme Court Justice Oliver Wendell Holmes, Jr.’s evocative description of the investor:

We are apt to think of ownership as a terminus, not as a gateway, and not to realize that except the tax levied for personal consumption large ownership means investment, and investment means the direction of labor towards the production of the greatest returns—returns that so far as they are great show by that very fact that they are consumed by the many, not alone by the few. … [T]he function of private ownership is to divine in advance the equilibrium of social desires—which socialism equally would have to divine, but which, under the illusion of self-seeking, is more poignantly and shrewdly foreseen [under capitalism]. …

The hated capitalist is simply the mediator, the prophet, the adjuster according to his divination of future desire. (Richard Posner [ed.], The Essential Holmes [Chicago: Chicago University Press, 1992], pp. 146-7)